The Debt Dilemma: How "Buy Now, Pay Later" Schemes Are Fueling a Global Crisis

June 14th, 2024 Latest Blogs

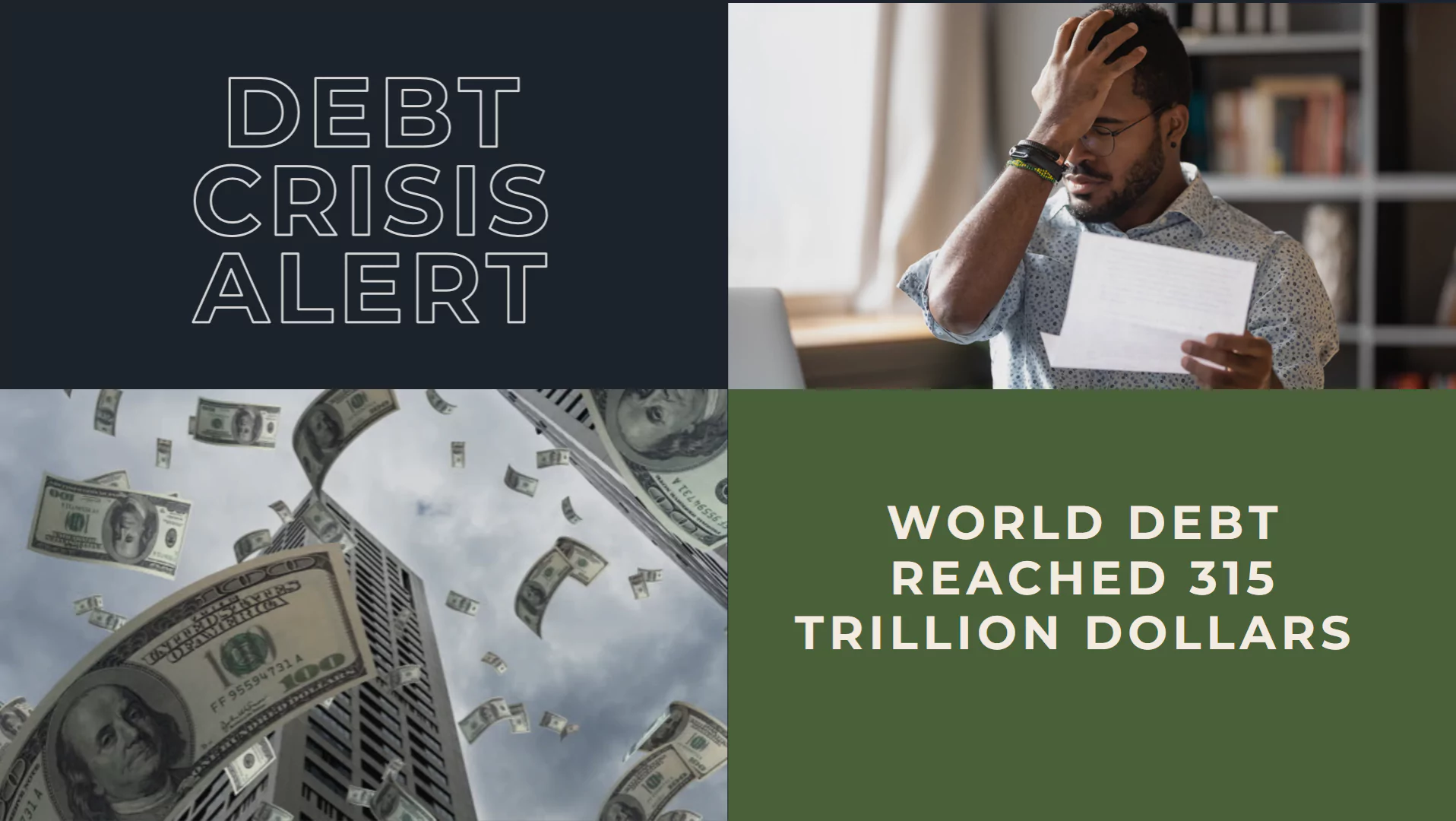

In today's world, the allure of "buy now, pay later" (BNPL) schemes is hard to resist. From everyday consumer goods to high-value assets like homes, the ease of acquiring debt has become a global phenomenon. However, this convenience comes with a heavy price. A recent news report from Firstpost highlights a staggering reality: the global debt has soared to an unprecedented $315 trillion, with a significant portion attributed to individual borrowings.

To put this into perspective, consider the following:

- - Global Debt: $315 trillion

- - Global Debt: $91 trillion

- - World Economy Valuation: $109 trillion

The numbers reveal a sobering fact: global debt is nearly three times the size of the world economy. This debt is not just held by governments and corporations but increasingly by individuals who are leveraging mortgages, home loans, and other forms of credit to sustain their lifestyles.

BNPL schemes have democratized access to credit, making it easier than ever for consumers to purchase goods and services without immediate payment. While this can drive economic activity, it also fosters a culture of instant gratification and deferred financial responsibility. The convenience of BNPL often masks the underlying accumulation of debt, leading many into financial precariousness.

Borge Brende, the President of the World Economic Forum, recently stated in an interview with Firstpost that never before in history have, we witnessed such high levels of debt. He highlighted that in most developing countries, interest payments have become a large part of national budgets. The sheer volume of debt is a ticking time bomb, with potential repercussions that could trigger a global recession. As interest rates rise and economic conditions tighten, the risk of defaults increases.

If a recession were to hit, the consequences could be devastating. Banks, under pressure to recoup losses, might begin foreclosing on homes, leading to widespread homelessness. This scenario echoes the subprime mortgage crisis of 2008 but on a potentially larger and more global scale.

The solution to this looming crisis lies in both individual and systemic changes. Individuals must cultivate financial prudence, prioritizing savings and responsible borrowing. At the same time, policymakers and financial institutions need to introduce measures that promote sustainable lending practices and protect consumers from the pitfalls of excessive debt.

As the world grapples with unprecedented levels of debt, the urgent need for financial responsibility and prudent economic policies has never been clearer. The path to stability requires a concerted effort from individuals, governments, and financial institutions alike. Only through collective action can we avert the catastrophic consequences of a debt-fueled recession and build a more secure financial future.

In conclusion, while the ease of "buy now, pay later" schemes offers short-term convenience, it is imperative to consider the long-term implications of accumulating debt. Financial literacy and responsibility, coupled with sound economic policies, are essential in navigating the current landscape and ensuring that the dream of ownership does not turn into a nightmare of foreclosure and financial ruin.